Low and Preceding High (Breakout + Bullis fgv + Extending Fib)🚀 Last Low & Preceding High: Bullish Reversal Strategy

This indicator identifies high-probability long setups by confirming a Bullish Market Structure Shift (BMS) coupled with a strong momentum filter.

🧠 Indicator Logic (How It Works)

The core function of this tool is to automatically locate the key structural points that lead to a bullish bias:

Structure Identification: It first defines a Range between the two most recent Pivot Lows. Within this range, it finds the Preceding High (the highest close before the current low) and the true Low Anchor (the lowest low/tail of the pivot low).

Breakout and Momentum Filter: A valid signal requires two conditions to be met on the current bar:

Bullish Breakout: The price must close above the Preceding High.

Marubozu Confirmation: A strong Bullish Marubozu candle (minimal wicks) must be present in the impulse move from the low, filtering for institutional strength.

Fibonacci Discount Zones: Upon confirmation, the indicator calculates and plots the discount zones (0.50, 0.618, 0.786) using the true extremes (tail-to-tail anchors). These zones start extending from the breakout candle and represent high-value areas for potential entries.

🎯 Entry and Risk Management

The strategy provides clear rules for execution once the logic is confirmed:

Entry Execution:

Wait for Retracement: Enter a Long position when the price retraces back into the colored Discount Zones (0.50 to 0.786).

Risk Control:

🛑 Stop Loss (SL): Placed below the Low Line (the swing low that initiated the move).

✅ Take Profit (TP): Placed above the High Line (the high that was broken).

Final note

"Special thanks to Mr. Mazen (@dr0chart) for developing this strategy."

Cari dalam skrip untuk "the strat"

Tristan's Tri-band StrategyTristan's Tri-band Strategy - Confluence Trading System

Strategy Overview:

This strategy combines three powerful technical indicators - RSI, Williams %R, and Bollinger Bands - into a single visual trading system. Instead of cluttering your chart with separate indicator panels, all signals are displayed directly on the price chart using color-coded gradient overlays, making it easy to spot high-probability trade setups at a glance.

How It Works:

The strategy identifies trading opportunities when multiple indicators align (confluence), suggesting strong momentum shifts:

📈 Long Entry Signals:

RSI drops to 30 or below (oversold)

Williams %R reaches -80 to -100 range (oversold)

Price touches or breaks below the lower Bollinger Band

All three conditions must align during your selected trading session

📉 Short Entry Signals:

RSI rises to 70 or above (overbought)

Williams %R reaches 0 to -20 range (overbought)

Price touches or breaks above the upper Bollinger Band

All three conditions must align during your selected trading session

Visual Indicators:

(faint) Green gradients below candles = Bullish oversold conditions (buying opportunity)

(faint) Red/Orange gradients above candles = Bearish overbought conditions (selling opportunity)

Stacked/brighter gradients = Multiple indicators confirming the same signal (higher probability) will stack and show brighter / less faint

Blue Bollinger Bands = Volatility boundaries and mean reversion zones

Exit Strategy:

Long trades exit when price reaches the upper Bollinger Band OR RSI becomes overbought (≥70)

Short trades exit when price reaches the lower Bollinger Band OR RSI becomes oversold (≤30)

Key Features:

✅ Session Filters - Trade only during NY (9:30 AM-4 PM), London (3 AM-11:30 AM), or Asia (7 PM-1 AM EST) sessions

✅ No Repainting - Signals are confirmed on candle close for realistic backtesting and live trading

✅ Customizable Parameters - Adjust RSI levels, BB standard deviations, Williams %R periods, and gradient visibility

✅ Visual Clarity - See all three indicators at once without switching between panels

✅ Built-in Alerts - Get notified when entry and exit conditions are met

How to Use Effectively:

Choose Your Trading Session - For day trading US stocks, enable only the NY session. For forex or 24-hour markets, select the sessions that match your schedule.

Look for Gradient Stacking - The brightest, most visible gradients occur when both RSI and Williams %R signal together. These are your highest-probability setups.

Confirm with Price Action - Wait for the candle to close before entering. The strategy enters on the next bar's open to prevent repainting.

Respect the Bollinger Bands - Entries occur at the outer bands (price extremes), and exits occur at the opposite band or when momentum reverses.

Backtest First - Test the strategy on your preferred instruments and timeframes. Works best on liquid assets with clear trends and mean reversion patterns (stocks, major forex pairs, indices).

Adjust Gradient Visibility - Use the "Gradient Strength" slider (lower = more visible) to make signals stand out on your chart style.

Best Timeframes: 5-minute to 1-hour charts for intraday trading; 4-hour to daily for swing trading (I have also found the 3 hour timeframe to work really well for some stocks / ETFs.)

Best Markets: Liquid instruments with volatility - SPY, QQQ, major stocks, EUR/USD, GBP/USD, major indices

Risk Management: This is a mean reversion strategy that works best in ranging or choppy markets. In strong trends, signals may appear less frequently. Always use proper position sizing and stop losses based on your risk tolerance.

----------------------------------------------

Note: Past performance does not guarantee future results. This strategy is provided for educational purposes. Always backtest thoroughly and practice proper risk management before live trading.RetryClaude can make mistakes. Please double-check responses. Sonnet 4.5

Buy&Hold Profitcalculator in EuroTitle: Buy & Hold Strategy in Euro

Description:

This Pine Script implements a simple yet flexible Buy & Hold strategy denominated in Euros, suitable for a wide range of assets including cryptocurrencies, forex pairs, and stocks.

Key Features:

Custom Investment Amount: Define your invested capital in Euros.

Flexible Start & End Dates: Specify exact entry and exit dates for the strategy.

Automatic Currency Conversion: Supports assets priced in USD or USDT, converting the invested capital to chart currency using the EUR/USD exchange rate.

Single Entry and Exit: Executes a one-time Buy & Hold position based on the defined timeframe.

Profit and Performance Tracking: Calculates total profit/loss in Euros and percentage returns.

Smart Exit Label: Displays a dynamic label at the exit showing final position value, net profit/loss, and return percentage. The label automatically adjusts its position above or below the price bar for optimal visibility.

Visual Enhancements:

Position value and profit/loss plotted on the chart.

Background color highlights the active investment period.

Buy and Sell markers clearly indicate entry and exit points.

This strategy is ideal for traders and investors looking to simulate long-term positions and evaluate performance in Euro terms, even when trading USD-denominated assets.

Usage Notes:

Best used on daily charts for medium- to long-term analysis.

Adjust start and end dates, as well as invested capital, to simulate different scenarios.

Works with any asset, but currency conversion is optimized for USD or USDT-pegged instruments.

v2.0—Tristan's Multi-Indicator Reversal Strategy🎯 Multi-Indicator Reversal Strategy - Optimized for High Win Rates

A powerful confluence-based strategy that combines RSI, MACD, Williams %R, Bollinger Bands, and Volume analysis to identify high-probability reversal points . Designed to let winners run with no stop loss or take profit - positions close only when opposite signals occur.

Also, the 3 hour timeframe works VERY well—just a lot less trades.

📈 Proven Performance

This strategy has been backtested and optimized on multiple blue-chip stocks with 80-90%+ win rates on 1-hour timeframes from Aug 2025 through Oct 2025:

✅ V (Visa) - Payment processor

✅ MSFT (Microsoft) - Large-cap tech

✅ WMT (Walmart) - Retail leader

✅ IWM (Russell 2000 ETF) - Small-cap index

✅ NOW (ServiceNow) - Enterprise software

✅ WM (Waste Management) - Industrial services

These stocks tend to mean-revert at extremes, making them ideal candidates for this reversal-based approach. I only list these as a way to show you the performance of the script. These values and stock choices may change over time as the market shifts. Keep testing!

🔑 How to Use This Strategy Successfully

Step 1: Apply to Chart

Open your desired stock (V, MSFT, WMT, IWM, NOW, WM recommended)

Set timeframe to 1 Hour

Apply this strategy

Check that the Williams %R is set to -20 and -80, and "Flip All Signals" is OFF (can flip this for some stocks to perform better.)

Step 2: Understand the Signals

🟢 Green Triangle (BUY) Below Candle:

Multiple indicators (RSI, Williams %R, MACD, Bollinger Bands) show oversold conditions

Enter LONG position

Strategy will pyramid up to 10 entries if more buy signals occur

Hold until red triangle appears

🔴 Red Triangle (SELL) Above Candle:

Multiple indicators show overbought conditions

Enter SHORT position (or close existing long)

Strategy will pyramid up to 10 entries if more sell signals occur

Hold until green triangle appears

🟣 Purple Labels (EXIT):

Shows when positions close

Displays count if multiple entries were pyramided (e.g., "Exit Long x5")

Step 3: Let the Strategy Work

Key Success Principles:

✅ Be Patient - Signals don't occur every day, wait for quality setups

✅ Trust the Process - Don't manually close positions, let opposite signals exit

✅ Watch Pyramiding - The strategy can add up to 10 positions in the same direction

✅ No Stop Loss - Positions ride through drawdowns until reversal confirmed

✅ Session Filter - Only trades during NY session (9:30 AM - 4:00 PM ET)

⚙️ Winning Settings (Already Set as Defaults)

INDICATOR SETTINGS:

- RSI Length: 14

- RSI Overbought: 70

- RSI Oversold: 30

- MACD: 12, 26, 9 (standard)

- Williams %R Length: 14

- Williams %R Overbought: -20 ⭐ (check this! And adjust to your liking)

- Williams %R Oversold: -80 ⭐ (check this! And adjust to your liking)

- Bollinger Bands: 20, 2.0

- Volume MA: 20 periods

- Volume Multiplier: 1.5x

SIGNAL REQUIREMENTS:

- Min Indicators Aligned: 2

- Require Divergence: OFF

- Require Volume Spike: OFF

- Require Reversal Candle: OFF

- Flip All Signals: OFF ⭐

RISK MANAGEMENT:

- Use Stop Loss: OFF ⭐⭐⭐

- Use Take Profit: OFF ⭐⭐⭐

- Allow Pyramiding: ON ⭐⭐⭐

- Max Pyramid Entries: 10 ⭐⭐⭐

SESSION FILTER:

- Trade Only NY Session: ON

- NY Session: 9:30 AM - 4:00 PM ET

**⭐ = Critical settings for success**

## 🎓 Strategy Logic Explained

### **How It Works:**

1. **Multi-Indicator Confluence**: Waits for at least 2 out of 4 technical indicators to align before generating signals

2. **Oversold = Buy**: When RSI < 30, Williams %R < -80, price below lower Bollinger Band, and/or MACD turning bullish → BUY signal

3. **Overbought = Sell**: When RSI > 70, Williams %R > -20, price above upper Bollinger Band, and/or MACD turning bearish → SELL signal

4. **Pyramiding Power**: As trend continues and more signals fire in the same direction, adds up to 10 positions to maximize gains

5. **Exit Only on Reversal**: No arbitrary stops or targets - only exits when opposite signal confirms trend change

6. **Session Filter**: Only trades during liquid NY session hours to avoid overnight gaps and low-volume periods

### **Why No Stop Loss Works:**

Traditional reversal strategies fail because they:

- Get stopped out too early during normal volatility

- Miss the actual reversal that happens later

- Cut winners short with tight take profits

This strategy succeeds because it:

- ✅ Rides through temporary noise

- ✅ Captures full reversal moves

- ✅ Uses multiple indicators for confirmation

- ✅ Pyramids into winning positions

- ✅ Only exits when technical picture completely reverses

---

## 📊 Understanding the Display

**Live Indicator Counter (Top Corner / end of current candles):**

Bull: 2/4

Bear: 0/4

(STANDARD)

Shows how many indicators currently align bullish/bearish

"STANDARD" = normal reversal mode (buy oversold, sell overbought)

"FLIPPED" = momentum mode if you toggle that setting

Visual Indicators:

🔵 Blue background = NY session active (trading window)

🟡 Yellow candle tint = Volume spike detected

💎 Aqua diamond = Bullish divergence (price vs RSI)

💎 Fuchsia diamond = Bearish divergence

⚡ Advanced Tips

Optimizing for Different Stocks:

If Win Rate is Low (<50%):

Try toggling "Flip All Signals" to ON (switches to momentum mode)

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Test on different timeframe (4-hour or daily)

If Too Few Signals:

Decrease "Min Indicators Aligned" to 2

Turn OFF all requirement filters

Widen Williams %R bands to -15 and -85

If Too Many False Signals:

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Turn ON "Require Volume Spike"

Reduce Max Pyramid Entries to 5

Stock Selection Guidelines:

Best Suited For:

Large-cap stable stocks (V, MSFT, WMT)

ETFs (IWM, SPY, QQQ)

Stocks with clear support/resistance

Mean-reverting instruments

Avoid:

Ultra low-volume penny stocks

Extremely volatile crypto (try traditional settings first)

Stocks in strong one-directional trends lasting months

🔄 The "Flip All Signals" Feature

If backtesting shows poor results on a particular stock, try toggling "Flip All Signals" to ON:

STANDARD Mode (OFF):

Buy when oversold (reversal strategy)

Sell when overbought

May work best for: V, MSFT, WMT, IWM, NOW, WM

FLIPPED Mode (ON):

Buy when overbought (momentum strategy)

Sell when oversold

May work best for: Strong trending stocks, momentum plays, crypto

Test both modes on your stock to see which performs better!

📱 Alert Setup

Create alerts to notify you of signals:

📊 Performance Expectations

With optimized settings on recommended stocks:

Typical results we are looking for:

Win Rate: 70-90%

Average Winner: 3-5%

Average Loser: 1-3%

Signals Per Week: 1-3 on 1-hour timeframe

Hold Time: Several hours to days

Remember: Past performance doesn't guarantee future results. Always use proper risk management.

Uptrick: Volume Weighted BandsIntroduction

This indicator, Uptrick: Volume Weighted Bands, overlays dynamic, volume-informed trend channels directly on the chart. By fusing price and volume data through volume-weighted and exponential moving averages, the script forms a core trend line with adaptive bandwidth controlled by volatility. It is designed to help traders identify trend direction, breakout entries, and extended conditions that may warrant take-profits or pullback re-entries.

Overview

The Volume Weighted Bands system is built around a trend line calculated by averaging a Volume Weighted Moving Average (VWMA) and an Exponential Moving Average (EMA), both over a configurable lookback period. This hybrid trend baseline is then smoothed further and expanded into dynamic upper and lower bands using an Average True Range (ATR) multiplier. These bands adapt with market volatility and shift color based on prevailing price action, helping traders quickly identify bullish, bearish, or neutral conditions.

Originality and Unique Features

This script introduces originality by blending both price and volume in the core trend calculation, a technique that is more responsive than traditional moving average bands. Its multi-mode visualization (cloud, single-band, or line-only), combined with selective buy/sell signals, makes it flexible for discretionary and algorithmic strategies alike. Optional modules for take-profit signals based on z-score deviation and RSI slope, as well as buy-back detection logic with cooldown filters, offer practical tools for managing trades beyond simple entries.

Explanation of Inputs

Every user input in this script is included to give the trader control over behavior and visual presentation:

Trend Length (len): Defines the lookback window for both the VWMA and EMA, controlling the sensitivity of the core trend baseline. A lower value makes the bands more reactive, while a higher value smooths out short-term noise.

Extra Smoothing (smoothLen): Applies an additional EMA to the blended VWMA/EMA average. This second-level smoothing ensures the central trend line reacts gradually to shifts in price.

Band Width (ATR Multiplier) (bandMult): Multiplies the ATR to create the width of the upper and lower bands around the trend line. Larger values widen the bands, capturing more volatility, while smaller values narrow them.

ATR Length (atrLen): Sets the length of the ATR used in calculating band width and signal offsets. Longer values produce smoother band boundaries.

Show Buy/Sell Signals (showSignals): Toggles the primary crossover/crossunder entry signals, which are labeled when the close crosses the upper or lower band.

Visual Mode (visualMode): Allows selection between three display modes:

--> Cloud: Shows both bands and the central trend line with a shaded background.

--> Single Band: Displays only the active (upper or lower) band depending on trend state, with gradient fill to price.

--> Line Only: Shows only the trend line for a minimal visual profile.

Take Profit Signals (enableTP): Enables a z-score-based profit-taking signal system. Signals occur when price deviates significantly from the trend line and RSI confirms exhaustion.

TP Z-Score Threshold (tpThreshold): Sets the z-score deviation required to trigger a take-profit signal. Higher values reduce the frequency of signals, focusing on more extreme moves.

Re-Entries (enableBuyBack): Enables logic to signal when price reverts into the band after an initial breakout, suggesting a possible re-entry or pullback setup.

Buy Back Cooldown (bars) (buyBackCooldown): Defines a minimum bar count before a new buy-back signal is allowed, preventing rapid retriggering in choppy conditions.

Buy Offset and Sell Offset: Hidden inputs used to vertically adjust the placement of the Buy ("𝓤𝓹") and Sell ("𝓓𝓸𝔀𝓷") labels relative to the bands. These use ATR units to maintain proportionality across different instruments and timeframes.

Take-Profit Signal Module

The take-profit module uses a z-score of the distance between price and the trend line to detect extended conditions. In bullish trends, a signal appears when price is well above the band and RSI indicates exhaustion; the opposite applies for bearish conditions. A boolean flag is used to prevent retriggering until RSI resets. These signals are plotted with minimalist “X” markers near recent highs or lows, based on whether the market is extended upward or downward.

Re-Entry Logic

The re-entry system identifies instances where price momentarily dips or spikes into the opposite band but closes back inside, implying a continuation of the prevailing trend. This module can be particularly useful for traders managing entries after brief pullbacks. A built-in cooldown period helps filter out noise and prevents signal overloading during fast markets. Visual markers are shown as upward or downward arrows near the relevant candle wicks.

How to Use This Indicator

The basic usage of this indicator follows a directional, signal-driven approach. When a buy signal appears, it suggests entering a long position. The recommended stop loss placement is below the lower band, allowing for some breathing space to accommodate natural volatility. As the position progresses, take partial profits—typically 10% to 15% of the position—each time a take-profit signal (marked with an "X") is shown on the chart.

An optional feature is the buy-back signal, which can be used to re-enter after partial exits or missed entries. Utilizing this can help reduce losses during false breakouts or trend reversals by scaling in more gradually. However, it also means that in strong, clean trends, the full position may not be captured from the start, potentially reducing the total return. It is up to the trader to decide whether to enter fully on the initial signal or incrementally using buy-backs.

When a sell signal appears, the strategy advises fully exiting any long positions and immediately switching to a short position. The short trade follows the same logic: place your stop loss above the upper band with some margin, and again, take partial profits at each take-profit signal.

Visual Presentation and Signal Labels

All signals are plotted with clean, minimal labels that avoid clutter, and are color-coded using a custom palette designed to remain clear across light and dark chart themes. Bullish trends are marked in teal and bearish trends in magenta. Candles and wicks are also colored accordingly to align price action with the detected trend state. Buy and sell entries are marked with "𝓤𝓹" and "𝓓𝓸𝔀𝓷" labels.

Summary

In summary, the Uptrick: Volume Weighted Bands indicator provides a versatile, visually adaptive trend and volatility tool that can serve multiple styles of trading. Through its integration of price, volume, and volatility, along with modular take-profit and buy-back signaling, it aims to provide actionable structure across a range of market conditions.

Disclaimer

This indicator is for educational purposes only. Trading involves risk, and past performance does not guarantee future results. Always test strategies before applying them in live markets.

Strat 3-Bar (Outside Bar) AlertThis indicator automatically detects and alerts you when a Strat 3-Bar (Outside Bar) forms on any chart or timeframe.

An Outside Bar (3) occurs when both sides of the previous candle’s range are taken out — the high breaks above the prior bar’s high AND the low breaks below its low. It signals expansion in price discovery and potential reversals or continuations.

📈 How to Use:

1. Add this script to your chart.

2. Look for red “3” labels or triangles above outside bars.

3. To get alerts, click the TradingView alert icon (⏰):

• Condition → Strat 3-Bar (Outside Bar) Alert

• Option → “Outside Bar (3) Detected”

• Choose “Once per bar close.”

💡 Pro Tips:

- Use with Strat Assist for visual context.

- Combine with timeframe continuity for directional bias.

- Great on 15-min, 1H, and Daily charts.

---

👩🏽💻 Shared with love by Yolanda

Inspired by community discussions with Jalen (ChatGPT)

Let’s keep building each other up and mastering The Strat together! 💛

TheStrat, outsidebar, 3bar, priceaction, tradingstrategy, alert, reversal, continuation, stratassist, strat, technicalanalysis, pinev6, smartmoney

Pullback Finder AutoPullback Finder Auto — Intraday Momentum Cooling Detector

Pullback Finder Auto is designed to find stocks that have made a strong intraday run from the open and are now cooling off while still positive — the classic pullback zone where continuation entries often form.

It automatically measures the percentage change from today’s open and highlights bars where:

the stock has already run at least a chosen amount (for example +10 % above its open), and

the current price is still up but within a defined pullback range (for example between +3 % and +8 % above the open).

When those two conditions are met, you’ll see green graphics on your chart:

Green triangle markers under the candle.

Optionally, small green PB labels such as “PB 5.2 %” showing the exact percentage from open when the setup occurs.

A green highlight in the sub‑window or line plot if you left the “Change from Open %” plot active.

These are your visual cues that a pullback has formed — a stock that previously ran and is now pulling back while holding strength.

How it works

The script continuously monitors:

• High % from Open = (high − open) / open × 100

• Current % from Open = (close − open) / open × 100

A “Pullback” condition triggers only if:

the high % is greater than or equal to your minimum run threshold, and

the current % sits between your minimum and maximum pullback percentages.

When both are true, the indicator plots the green triangle and optional label.

Default parameters

Min Run % = 10

Min Current % = 3

Max Current % = 8

Session Start = 09:30 – 16:00 US Eastern

All can be changed to fit different volatility levels.

Lower values catch smaller moves; higher values restrict signals to explosive runners.

Using it in real time

During live trading, Pullback Finder Auto updates with each candle.

When a bar first enters the target zone, a green triangle and PB label will appear immediately under that candle.

These are dynamic: if price moves out of the valid zone on the same bar, the marker may disappear.

You can create an alert on “Pullback Finder Auto – Pullback Candidate” to be notified whenever new triangles appear across your active symbols.

This works on any timeframe:

use shorter timeframes such as 1‑minute or 5‑minute charts for fast, intraday detection,

use longer timeframes for a broader view of the day’s market structure.

Using it on past data (scanning backwards)

When you scroll back through history, past green triangles remain visible at every bar where the condition was true at that time.

The PB labels next to those candles show exactly how far above the open the stock was trading during the historical setup.

Use this for visual back‑testing: study how price reacted after these pullback points, adjust the thresholds, and refine your criteria for different markets.

The grey or teal line under the chart (if enabled) shows the percent‑from‑open curve so you can see the full run‑and‑cool pattern leading into each triangle signal.

If you convert the indicator into a strategy, the same condition becomes historical entry points you can test with the Strategy Tester.

Summary

1. Pullback Finder Auto paints green triangles and PB labels whenever an intraday pullback fits your criteria.

2. It runs dynamically in real‑time and also preserves markers for historical review.

3. Adjust the thresholds to match volatility or timeframe.

4. Ideal for visual scanning, watchlist alerts, or integration into a lightweight screening strategy.

Adaptive Trend 1m ### Overview

The "Adaptive Trend Impulse Parallel SL/TP 1m Realistic" strategy is a sophisticated trading system designed specifically for high-volatility markets like cryptocurrencies on 1-minute timeframes. It combines trend-following with momentum filters and adaptive parameters to dynamically adjust to market conditions, ensuring more reliable entries and risk management. This strategy uses SuperTrend for primary trend detection, enhanced by MACD, RSI, Bollinger Bands, and optional volume spikes. It incorporates parallel stop-loss (SL) and multiple take-profit (TP) levels based on ATR, with options for breakeven and trailing stops after the first TP. Optimized for realistic backtesting on short timeframes, it avoids over-optimization by adapting indicators to market speed and efficiency.

### Principles of Operation

The strategy operates on the principle of adaptive impulse trading, where entry signals are generated only when multiple conditions align to confirm a strong trend reversal or continuation:

1. **Trend Detection (SuperTrend)**: The core signal comes from an adaptive SuperTrend indicator. It calculates upper and lower bands using ATR (Average True Range) with dynamic periods and multipliers. A buy signal occurs when the price crosses above the lower band (from a downtrend), and a sell signal when it crosses below the upper band (from an uptrend). Adaptation is based on Rate of Change (ROC) to measure market speed, shortening periods in fast markets for quicker responses.

2. **Momentum and Trend Filters**:

- **MACD**: Uses adaptive fast and slow lengths. In "Trend Filter" mode (default when "Use MACD Cross" is false), it checks if the MACD line is above/below the signal for long/short. In cross mode, it requires a crossover/crossunder.

- **RSI**: Adaptive period RSI must be above 50 for longs and below 50 for shorts, confirming overbought/oversold conditions dynamically.

- **Bollinger Bands (BB)**: Depending on the mode ("Midline" by default), it requires the price to be above/below the BB midline for longs/shorts, or a breakout in "Breakout" mode. Deviation adapts to market efficiency.

- **Volume Spike Filter** (optional): Entries require volume to exceed an adaptive multiple of its SMA, signaling strong impulse.

3. **Volatility Filter**: Entries are only allowed if current ATR percentage exceeds a historical minimum (adaptive), preventing trades in low-volatility ranges.

4. **Risk Management (Parallel SL/TP)**:

- **Stop-Loss**: Set at an adaptive ATR multiple below/above entry for long/short.

- **Take-Profits**: Three levels at adaptive ATR multiples, with partial position closures (e.g., 51% at TP1, 25% at TP2, remainder at TP3).

- **Post-TP1 Features**: Optional breakeven moves SL to entry after TP1. Trailing SL uses BB midline as a dynamic trail.

- All levels are calculated per trade using the ATR at entry, making them "realistic" for 1m charts by widening SL and tightening initial TPs.

The strategy enters long on buy signals with all filters met, and short on sell signals. It uses pyramid margin (100% long/short) for full position sizing.

Adaptation is driven by:

- **Market Speed (normSpeed)**: Based on ROC, tightens multipliers in volatile periods.

- **Efficiency Ratio (ER)**: Measures trend strength, adjusting periods for trending vs. ranging markets.

This ensures the strategy "adapts" without manual tweaks, reducing false signals in varying conditions.

### Main Advantages

- **Adaptability**: Unlike static strategies, parameters dynamically adjust to market volatility and trend strength, improving performance across ranging and trending phases without over-optimization.

- **Realistic Risk Management for 1m**: Wider SL and tiered TPs prevent premature stops in noisy short-term charts, while partial profits lock in gains early. Breakeven/trailing options protect profits in extended moves.

- **Multi-Filter Confirmation**: Combines trend, momentum, and volume for high-probability entries, reducing whipsaws. The volatility filter avoids flat markets.

- **Debug Visualization**: Built-in plots for signals, levels, and component checks (when "Show Debug" is enabled) help users verify logic on charts.

- **Efficiency**: Low computational load, suitable for real-time trading on TradingView with alerts.

Backtesting shows robust results on volatile assets, with a focus on sustainable risk (e.g., SL at 3x ATR avoids excessive drawdowns).

### Uniqueness

What sets this strategy apart is its **fully adaptive framework** integrating multiple indicators with real-time market metrics (ROC for speed, ER for efficiency). Most trend strategies use fixed parameters, leading to poor adaptation; here, every key input (periods, multipliers, deviations) scales dynamically within bounds, creating a "self-tuning" system. The "parallel SL/TP with 1m realism" adds custom handling for micro-timeframes: tightened initial TPs for quick wins and adaptive min-ATR filter to skip low-vol bars. Unlike generic mashups, it justifies the combination—SuperTrend for trend, MACD/RSI/BB for impulse confirmation, volume for conviction—working synergistically to capture "trend impulses" while filtering noise. The post-TP1 breakeven/trailing tied to BB adds a unique profit-locking mechanism not common in open-source scripts.

### Recommended Settings

These settings are optimized and recommended for trading ASTER/USDT on Bybit, with 1-minute chart, x10 leverage, and cross margin mode. They provide a balanced risk-reward for this volatile pair:

- **Base Inputs**:

- Base ATR Period: 10

- Base SuperTrend ATR Multiplier: 2.5

- Base MACD Fast: 8

- Base MACD Slow: 17

- Base MACD Signal: 6

- Base RSI Period: 9

- Base Bollinger Period: 12

- Bollinger Deviation: 1.8

- Base Volume SMA Period: 19

- Base Volume Spike Multiplier: 1.8

- Adaptation Window: 54

- ROC Length: 10

- **TP/SL Settings**:

- Use Stop Loss: True

- Base SL Multiplier (ATR): 3

- Use Take Profits: True

- Base TP1 Multiplier (ATR): 5.5

- Base TP2 Multiplier (ATR): 10.5

- Base TP3 Multiplier (ATR): 19

- TP1 % Position: 51

- TP2 % Position: 25

- Breakeven after TP1: False

- Trailing SL after TP1: False

- Base Min ATR Filter: 0.001

- Use Volume Spike Filter: True

- BB Condition: Midline

- Use MACD Cross (false=Trend Filter): True

- Show Debug: True

For backtesting, use initial capital of 30 USD, base currency USDT, order size 100 USDT, pyramiding 1, commission 0.1%, slippage 0 ticks, long/short margin 0%.

Always backtest on your platform and use risk management—risk no more than 1-2% per trade. This is not financial advice; trade at your own risk.

4-Hour Range Scalping [v6.3]User Guide: 4-Hour Range Scalping Strategy

Hello! Here is the guide for the Pine Script strategy. Please read it carefully to get the best results.

📈 This script automates the "4-Hour Range Scalping Strategy" from the video.

The main idea is that the first four hours of a major trading day (like New York) set up a "trap zone." The strategy waits for the price to break out of this zone and then fail, giving us a signal that the breakout was false and the price is likely to reverse.

Here’s the simple logic:

Define the Range: It precisely calculates the highest high and lowest low during the first four hours of the selected trading session (e.g., 00:00 to 04:00 New York Time).

Wait for a Breakout: It then monitors the 5-minute chart for a price breakout where a candle fully closes outside of this established range.

Identify the Reversal: The trade trigger occurs when the price fails to continue its breakout and a subsequent 5-minute candle closes back inside the range. This signals a potential reversal or "failed breakout."

Execute the Trade:

]A Short (Sell) trade is triggered after a failed breakout above the range high.

A Long (Buy) trade is triggered after a failed breakout below the range low.

Manage the Risk: The Stop Loss is automatically placed at the peak (for shorts) or trough (for longs) of the breakout move, and the Take Profit is set to a default 2:1 Risk/Reward Ratio.

How to Use the Script (Step-by-Step) ⚙️

Follow these instructions to get it running perfectly.

1. Set Your Chart Timeframe This is the most important step. The strategy is designed to run on a 5-minute (5m) chart. Open your TradingView chart and make sure the timeframe is set to "5m".

2. Add the Script to Your Chart Open the Pine Editor tab at the bottom of TradingView, paste the entire script, and click the "Add to chart" button.

3. Configure the Settings On your chart, find the strategy's name (e.g., "4-Hour Range Scalping ") and click the gear icon ⚙️ to open its settings.

Trading Session: Choose the session for the range. New York is the default and the one from the video.

Risk/Reward Ratio: The default is 2.0, meaning your potential profit is twice your potential loss. You can adjust this to test other targets.

Backtesting Period: To see how the strategy performed on all historical data, go to the "Strategy Tester" panel, click its own gear icon ⚙️, and uncheck the boxes for "Start Date" and "End Date."

4. Understand the Visuals on Your Chart

Blue Background Area: This is the 4-hour calculation window. The script is identifying the day's high and low during this time. No trades will ever happen here.

Red Line (Range High): The highest price of the 4-hour window. This is the upper boundary of the "trap zone."

Green Line (Range Low): The lowest price of the 4-hour window. This is the lower boundary.

Green Triangle (▲): Shows where a Long (Buy) trade was entered.

Red Triangle (▼): Shows where a Short (Sell) trade was entered.

A Very Important Note on Timezones 🕒

This is critical for you in the Philippines (PHT).

The script is based on the New York session, which is 12 hours behind you. Your TradingView chart will still show your local time, but the script works on NY time in the background.

The New York "day" begins at 12:00 PM (Noon) your time.

The script's blue calculation window will be from 12:00 PM to 4:00 PM your local time.

The red and green range lines will appear on your chart only after 4:00 PM your time.

So, if you look at your chart in the morning or early afternoon, you will not see today's range yet. This is normal! The script is just waiting for the New York session to start.

How to Set Up Trade Alerts 🔔

You can have TradingView send you a notification whenever the script enters a trade.

Click the "Alert" button (looks like a clock) in the right-hand toolbar of TradingView.

In the "Condition" dropdown, select the name of the script (e.g., "4-Hour Range Scalping...").

You will then see two options: "Long Signal" and "Short Signal".

Select one (e.g., "Long Signal") and configure how you want to be notified (e.g., "Notify on app").

Click "Create". Repeat the process to create an alert for the other signal.

⚠️ Important Disclosure

For Educational and Research Purposes Only.

This script and all accompanying information are provided for educational and research purposes only. The strategy demonstrated is a technical concept and should not be misconstrued as financial, investment, legal, or tax advice.

Trading financial markets involves substantial risk and is not suitable for every investor. There is a possibility that you could sustain a loss of some or all of your initial investment. Therefore, you should not invest money that you cannot afford to lose.

Past performance is not indicative of future results. The backtesting results shown by this script are historical and do not guarantee future performance. Market conditions are constantly changing.

By using this script, you acknowledge that you are solely responsible for any and all trading decisions you make. You should conduct your own thorough research and, if necessary, seek advice from an independent financial advisor before making any investment decisions. The creators of this script assume no liability for any of your trading results.

HermesHERMES STRATEGY - TRADINGVIEW DESCRIPTION

OVERVIEW

Hermes is an adaptive trend-following strategy that uses dual ALMA (Arnaud Legoux Moving Average) filters to identify high-quality entry and exit points. It's designed for swing and position traders who want smooth, low-lag signals with minimal whipsaws.

Unlike traditional moving averages that operate on price, Hermes analyzes price returns (percentage changes) to create signals that work consistently across any asset class and price range.

HOW IT WORKS

DUAL ALMA SYSTEM

The strategy uses two ALMA lines applied to price returns:

• Fast ALMA (Blue Line): Short-term trend signal (default: 80 periods)

• Slow ALMA (Black Line): Long-term baseline trend (default: 250 periods)

ALMA is superior to simple or exponential moving averages because it provides:

• Smoother curves with less noise

• Significantly reduced lag

• Natural resistance to outliers and flash crashes

TRADING LOGIC

BUY SIGNAL:

• Fast ALMA crosses above Slow ALMA (bullish regime)

• Price makes new N-bar high (momentum confirmation)

• Optional: Price above 200 EMA (macro trend filter)

• Optional: ALMA lines sufficiently separated (strength filter)

SELL SIGNAL:

• Fast ALMA crosses below Slow ALMA (bearish regime)

• Optional: Price makes new N-bar low (momentum confirmation)

The strategy stays in position during the entire bullish regime, allowing you to ride trends for weeks or months.

VISUAL INDICATORS

LINES:

• Blue Line: Fast ALMA (short-term signal)

• Black Line: Slow ALMA (long-term baseline)

TRADE MARKERS:

• Green Triangle Up: Buy executed

• Red Triangle Down: Sell executed

• Orange "M": Buy blocked by momentum filter

• Purple "W": Buy blocked by weak crossover strength

KEY PARAMETERS

ALMA SETTINGS:

• Short Period (default: 30) - Fast signal responsiveness

• Long Period (default: 250) - Baseline stability

• ALMA Offset (default: 0.90) - Balance between lag and smoothness

• ALMA Sigma (default: 7.5) - Gaussian curve width

ENTRY/EXIT FILTERS:

• Buy Lookback (default: 7) - Bars for momentum confirmation (required)

• Sell Lookback (default: 0) - Exit momentum bars (0 = disabled for faster exits)

• Min Crossover Strength (default: 0.0) - Required ALMA separation (0 = disabled)

• Use Macro Filter (default: true) - Only enter above 200 EMA

BEST PRACTICES

RECOMMENDED ASSETS - Works well on:

• Cryptocurrencies (Bitcoin, Ethereum, etc.)

• Major indices (S&P 500, Nasdaq)

• Large-cap stocks

• Commodities (Gold, Oil)

RECOMMENDED TIMEFRAMES:

• Daily: Primary timeframe for swing trading

• 4-Hour: More active trading (increase trade frequency)

• Weekly: Long-term position trading

PARAMETER TUNING:

• More trades: Lower Short Period (60-80)

• Fewer trades: Raise Short Period (100-120)

• Faster exits: Set Sell Lookback = 0

• Safer entries: Enable Macro Filter (Use Macro Filter = true)

STRATEGY ADVANTAGES

1. Low Lag - ALMA provides faster signals than traditional moving averages

2. Smooth Signals - Minimal whipsaws compared to crossover strategies

3. Asset Agnostic - Same parameters work across different markets

4. Trend Capture - Stays positioned during entire bullish regimes

5. Risk Management - Multiple filters prevent poor entries

6. Visual Clarity - Easy to interpret regime and filter states

WHEN TO USE HERMES

BEST FOR:

• Trending markets (crypto bull runs, equity uptrends)

• Swing trading (hold days to weeks)

• Position trading (hold weeks to months)

• Clear trend identification

• Risk-managed exposure

NOT SUITABLE FOR:

• Ranging/sideways markets

• Scalping or day trading

• High-frequency trading

• Mean reversion strategies

RISK DISCLAIMER

This indicator is for educational purposes only. Past performance does not guarantee future results. Always use proper position sizing and risk management. Test thoroughly on historical data before live trading.

CREDITS

Inspired by Giovanni Santostasi's Power Law Volatility Indicator, generalized for universal application across all assets using adaptive ALMA filtering.

Strategy by Hermes Trading Systems

QUICK START

1. Add indicator to chart

2. Use on daily timeframe for best results

3. Look for green buy signals when blue line crosses above black line

4. Exit on red sell signals when blue line crosses below black line

5. Adjust parameters based on your trading style:

• Conservative: Enable Macro Filter, increase Buy Lookback to 10

• Aggressive: Disable Macro Filter, lower Short Period to 60

• Default settings work well for most assets

AlgoWay GRSIM🧭 What this strategy tries to do

This strategy detects when a market move is losing strength and prepares for a potential reversal, but it waits for fresh momentum confirmation before acting.

It combines:

• RSI-based divergence (to spot exhaustion and potential turning points),

• Impulse MACD (to verify that the new direction actually has force behind it).

________________________________________

⚙️ When it takes trades

Long (Buy):

• A bullish RSI divergence appears (a clue that selling pressure is fading);

• Within a short time window, the Impulse MACD turns strongly positive;

• Optionally, the impulse line itself must be rising (if the Impulse Direction Filter is

enabled).

Short (Sell):

• A bearish RSI divergence appears (buying pressure fading);

• Within a short time window, the Impulse MACD turns strongly negative;

• Optionally, the impulse line must be falling (if the Impulse Direction Filter is enabled).

If momentum confirmation happens too late, the divergence “expires” and the signal is ignored.

________________________________________

🧩 How entries work

1. Reversal clue:

The strategy detects disagreement between price and RSI (price makes a new high/low, RSI doesn’t).

That suggests a shift in underlying strength.

2. Momentum confirmation:

Before entering, the Impulse MACD must agree — showing real push in the same direction.

3. Impulse direction filter (optional):

When enabled, the impulse itself must accelerate (rise for longs, fall for shorts), avoiding fake signals where price diverges but momentum is still fading.

4. No stacking:

It opens only one position at a time.

________________________________________

🚪 How exits work

Two main exit styles:

Conservative (default):

Longs close when impulse crosses below its signal line.

Shorts close when impulse crosses above its signal line.

✅ Keeps trades as long as momentum agrees.

Color-change (fast):

Longs close immediately when impulse flips bearish.

Shorts close immediately when impulse flips bullish.

⚡ Faster and more defensive.

Plus:

Stop Loss (%) and Take Profit (%) act as fixed-distance protective exits (set to 0 to disable either one).

________________________________________

📊 What you’ll see on the chart

A thick Impulse MACD line and thin signal line (oscillator view).

Diamonds — detected bullish/bearish divergence points.

Circles — where impulse crosses its signal (momentum change).

A performance panel (top-right) showing Net Profit, Trades, Win Rate, Profit Factor, Pessimistic PF, and Max Drawdown.

________________________________________

🔧 What you can tune

Signal Lifetime (bars): how long a divergence remains valid.

Impulse Direction Filter: ensure the impulse itself is moving in the trade’s direction.

Stop Loss / Take Profit (%): risk and target in percent.

Exit Style: conservative cross or faster color-change.

RSI / MA / Signal Lengths: adjust responsiveness (defaults are balanced).

________________________________________

💪 Strengths

Confirms reversals using momentum direction, not just divergence.

Avoids “early” signals where momentum is still fading.

Works symmetrically for longs and shorts.

Built-in stop/target protection.

Clear, visual confirmation of all logic components.

________________________________________

⚠️ Things to keep in mind

In sideways markets, the impulse can flip often — prefer conservative exits.

Too small SL/TP → constant stop-outs.

Too wide SL/TP → deep drawdowns.

Always test with different timeframes and markets.

________________________________________

💡 Practical tips

Start with default settings.

Enable “Use Impulse Direction Filter” in trending markets, disable it in very choppy ones.

Focus on Profit Factor, Win Rate, and Max Drawdown after several dozen trades.

Keep SL/TP roughly aligned with typical swing size.

“AlgoWay GRSIM” is a reversal-with-confirmation strategy: it spots likely turns, demands real momentum alignment (optionally verified by impulse direction), and manages exits with clear momentum cues plus built-in protective limits.

Quantum Flux Universal Strategy Summary in one paragraph

Quantum Flux Universal is a regime switching strategy for stocks, ETFs, index futures, major FX pairs, and liquid crypto on intraday and swing timeframes. It helps you act only when the normalized core signal and its guide agree on direction. It is original because the engine fuses three adaptive drivers into the smoothing gains itself. Directional intensity is measured with binary entropy, path efficiency shapes trend quality, and a volatility squash preserves contrast. Add it to a clean chart, watch the polarity lane and background, and trade from positive or negative alignment. For conservative workflows use on bar close in the alert settings when you add alerts in a later version.

Scope and intent

• Markets. Large cap equities and ETFs. Index futures. Major FX pairs. Liquid crypto

• Timeframes. One minute to daily

• Default demo used in the publication. QQQ on one hour

• Purpose. Provide a robust and portable way to detect when momentum and confirmation align, while dampening chop and preserving turns

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique concept or fusion. The novelty sits in the gain map. Instead of gating separate indicators, the model mixes three drivers into the adaptive gains that power two one pole filters. Directional entropy measures how one sided recent movement has been. Kaufman style path efficiency scores how direct the path has been. A volatility squash stabilizes step size. The drivers are blended into the gains with visible inputs for strength, windows, and clamps.

• What failure mode it addresses. False starts in chop and whipsaw after fast spikes. Efficiency and the squash reduce over reaction in noise.

• Testability. Every component has an input. You can lengthen or shorten each window and change the normalization mode. The polarity plot and background provide a direct readout of state.

• Portable yardstick. The core is normalized with three options. Z score, percent rank mapped to a symmetric range, and MAD based Z score. Clamp bounds define the effective unit so context transfers across symbols.

Method overview in plain language

The strategy computes two smoothed tracks from the chart price source. The fast track and the slow track use gains that are not fixed. Each gain is modulated by three drivers. A driver for directional intensity, a driver for path efficiency, and a driver for volatility. The difference between the fast and the slow tracks forms the raw flux. A small phase assist reduces lag by subtracting a portion of the delayed value. The flux is then normalized. A guide line is an EMA of a small lead on the flux. When the flux and its guide are both above zero, the polarity is positive. When both are below zero, the polarity is negative. Polarity changes create the trade direction.

Base measures

• Return basis. The step is the change in the chosen price source. Its absolute value feeds the volatility estimate. Mean absolute step over the window gives a stable scale.

• Efficiency basis. The ratio of net move to the sum of absolute step over the window gives a value between zero and one. High values mean trend quality. Low values mean chop.

• Intensity basis. The fraction of up moves over the window plugs into binary entropy. Intensity is one minus entropy, which maps to zero in uncertainty and one in very one sided moves.

Components

• Directional Intensity. Measures how one sided recent bars have been. Smoothed with RMA. More intensity increases the gain and makes the fast and slow tracks react sooner.

• Path Efficiency. Measures the straightness of the price path. A gamma input shapes the curve so you can make trend quality count more or less. Higher efficiency lifts the gain in clean trends.

• Volatility Squash. Normalizes the absolute step with Z score then pushes it through an arctangent squash. This caps the effect of spikes so they do not dominate the response.

• Normalizer. Three modes. Z score for familiar units, percent rank for a robust monotone map to a symmetric range, and MAD based Z for outlier resistance.

• Guide Line. EMA of the flux with a small lead term that counteracts lag without heavy overshoot.

Fusion rule

• Weighted sum of the three drivers with fixed weights visible in the code comments. Intensity has fifty percent weight. Efficiency thirty percent. Volatility twenty percent.

• The blend power input scales the driver mix. Zero means fixed spans. One means full driver control.

• Minimum and maximum gain clamps bound the adaptive gain. This protects stability in quiet or violent regimes.

Signal rule

• Long suggestion appears when flux and guide are both above zero. That sets polarity to plus one.

• Short suggestion appears when flux and guide are both below zero. That sets polarity to minus one.

• When polarity flips from plus to minus, the strategy closes any long and enters a short.

• When flux crosses above the guide, the strategy closes any short.

What you will see on the chart

• White polarity plot around the zero line

• A dotted reference line at zero named Zen

• Green background tint for positive polarity and red background tint for negative polarity

• Strategy long and short markers placed by the TradingView engine at entry and at close conditions

• No table in this version to keep the visual clean and portable

Inputs with guidance

Setup

• Price source. Default ohlc4. Stable for noisy symbols.

• Fast span. Typical range 6 to 24. Raising it slows the fast track and can reduce churn. Lowering it makes entries more reactive.

• Slow span. Typical range 20 to 60. Raising it lengthens the baseline horizon. Lowering it brings the slow track closer to price.

Logic

• Guide span. Typical range 4 to 12. A small guide smooths without eating turns.

• Blend power. Typical range 0.25 to 0.85. Raising it lets the drivers modulate gains more. Lowering it pushes behavior toward fixed EMA style smoothing.

• Vol window. Typical range 20 to 80. Larger values calm the volatility driver. Smaller values adapt faster in intraday work.

• Efficiency window. Typical range 10 to 60. Larger values focus on smoother trends. Smaller values react faster but accept more noise.

• Efficiency gamma. Typical range 0.8 to 2.0. Above one increases contrast between clean trends and chop. Below one flattens the curve.

• Min alpha multiplier. Typical range 0.30 to 0.80. Lower values increase smoothing when the mix is weak.

• Max alpha multiplier. Typical range 1.2 to 3.0. Higher values shorten smoothing when the mix is strong.

• Normalization window. Typical range 100 to 300. Larger values reduce drift in the baseline.

• Normalization mode. Z score, percent rank, or MAD Z. Use MAD Z for outlier heavy symbols.

• Clamp level. Typical range 2.0 to 4.0. Lower clamps reduce the influence of extreme runs.

Filters

• Efficiency filter is implicit in the gain map. Raising efficiency gamma and the efficiency window increases the preference for clean trends.

• Micro versus macro relation is handled by the fast and slow spans. Increase separation for swing, reduce for scalping.

• Location filter is not included in v1.0. If you need distance gates from a reference such as VWAP or a moving mean, add them before publication of a new version.

Alerts

• This version does not include alertcondition lines to keep the core minimal. If you prefer alerts, add names Long Polarity Up, Short Polarity Down, Exit Short on Flux Cross Up in a later version and select on bar close for conservative workflows.

Strategy has been currently adapted for the QQQ asset with 30/60min timeframe.

For other assets may require new optimization

Properties visible in this publication

• Initial capital 25000

• Base currency Default

• Default order size method percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Honest limitations and failure modes

• Past results do not guarantee future outcomes

• Economic releases, circuit breakers, and thin books can break the assumptions behind intensity and efficiency

• Gap heavy symbols may benefit from the MAD Z normalization

• Very quiet regimes can reduce signal contrast. Use longer windows or higher guide span to stabilize context

• Session time is the exchange time of the chart

• If both stop and target can be hit in one bar, tie handling would matter. This strategy has no fixed stops or targets. It uses polarity flips for exits. If you add stops later, declare the preference

Open source reuse and credits

• None beyond public domain building blocks and Pine built ins such as EMA, SMA, standard deviation, RMA, and percent rank

• Method and fusion are original in construction and disclosure

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Strategy add on block

Strategy notice

Orders are simulated by the TradingView engine on standard candles. No request.security() calls are used.

Entries and exits

• Entry logic. Enter long when both the normalized flux and its guide line are above zero. Enter short when both are below zero

• Exit logic. When polarity flips from plus to minus, close any long and open a short. When the flux crosses above the guide line, close any short

• Risk model. No initial stop or target in v1.0. The model is a regime flipper. You can add a stop or trail in later versions if needed

• Tie handling. Not applicable in this version because there are no fixed stops or targets

Position sizing

• Percent of equity in the Properties panel. Five percent is the default for examples. Risk per trade should not exceed five to ten percent of equity. One to two percent is a common choice

Properties used on the published chart

• Initial capital 25000

• Base currency Default

• Default order size percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Dataset and sample size

• Test window Jan 2, 2014 to Oct 16, 2025 on QQQ one hour

• Trade count in sample 324 on the example chart

Release notes template for future updates

Version 1.1.

• Add alertcondition lines for long, short, and exit short

• Add optional table with component readouts

• Add optional stop model with a distance unit expressed as ATR or a percent of price

Notes. Backward compatibility Yes. Inputs migrated Yes.

STRAT Pattern Scanner - All 22 PatternsSTRAT Candle call outs. A learning tool created to help me identify different STRAT candle types while learning The STRAT strategy designed by the late Rob Smith. Feel free to change the code or add to it for personalized use.

Bitcoin Halving Strategy

A systematic, data-driven trading strategy based on Bitcoin's 4-year halving cycles. This strategy capitalizes on historical price patterns that emerge around halving events, providing clear entry and exit signals for both accumulation and profit-taking phases.

🎯 Strategy Overview

This automated trading system identifies optimal buy and sell zones based on the predictable Bitcoin halving cycle that occurs approximately every 4 years. By analyzing historical data from all previous halvings (2012, 2016, 2020, 2024), the strategy pinpoints high-probability trading opportunities.

📊 Key Features

Automated Signal Generation: Buy signals at halving events and DCA zones, sell signals at profit-taking peaks

Multi-Phase Analysis: Tracks Accumulation, Profit Taking, Bear Market, and DCA phases

Visual Dashboard: Real-time performance metrics, phase countdown, and position tracking

Backtesting Enabled: Comprehensive historical performance analysis with configurable parameters

Risk Management: Built-in position sizing, slippage control, and optional short trading

⚙️ Strategy Logic

Buy Signals:

At halving event (Week 0)

DCA zone entry (Week 135 post-halving)

Sell Signals:

Profit-taking zone (Week 80 post-halving)

Optional short position entry for advanced traders

📈 Performance Highlights

Captures major bull run profits while avoiding prolonged bear markets

Clear visual indicators for all phases and transitions

Customizable timing parameters for personalized risk tolerance

Professional dashboard with live P&L, win rate, and drawdown metrics

🛠️ Customization Options

Adjustable phase timing (profit start/end, DCA timing)

Position sizing control

Enable/disable short trading

Visual customization (colors, labels, zones)

Table positioning and transparency

⚠️ Risk Disclosure

Past performance does not guarantee future results. This strategy is based on historical halving cycle patterns and should be used as part of a comprehensive trading plan. Always conduct your own research and consider your risk tolerance before trading.

💡 Ideal For

Long-term Bitcoin investors seeking systematic entry/exit points

Swing traders capitalizing on multi-month trends

Portfolio managers implementing cycle-based allocation strategies

RSI Momentum ScalperOverview

The "RSI Momentum Scalper" is a Pine Script v5 strategy crafted for trading highly volatile markets, with a special focus on newly listed cryptocurrencies. This strategy harnesses the Relative Strength Index (RSI) alongside volume analysis and momentum thresholds to pinpoint short-term trading opportunities. It supports both long and short trades, managed with customizable take profit, stop loss, and trailing stop levels, which are visually plotted on the chart for easy tracking.

Why I Created This Strategy

I developed the "RSI Momentum Scalper" because I was seeking a reliable trading strategy tailored to newly listed, highly volatile cryptocurrencies. These assets often experience rapid price fluctuations, rendering traditional strategies less effective. I aimed to create a tool that could exploit momentum and volume spikes while managing risk through adaptable exit parameters. This strategy is designed to address that need, offering a flexible approach for traders in dynamic crypto markets.

How It Works

The strategy utilizes RSI to identify momentum shifts, combined with volume confirmation, to trigger long or short entries. Trades are controlled with take profit, stop loss, and trailing stop levels, which adjust dynamically as the price moves in your favor. The trailing stop helps lock in profits, while the plotted exit levels provide clear visual cues for trade management.

Customizable Settings

The script is highly customizable, allowing you to adjust it to various market conditions and trading styles. Here’s a brief overview of the key settings:

Trade Mode: Select "Both," "Long Only," or "Short Only" to determine the trade direction.

(Default: Both)

RSI Length: Sets the lookback period for the RSI calculation (2 to 30).

(Default: 8)

A shorter length increases RSI sensitivity, suitable for volatile assets.

RSI Overbought: Defines the upper RSI threshold (60 to 99) for short entries.

(Default: 90)

Higher values signal stronger overbought conditions.

RSI Oversold: Defines the lower RSI threshold (1 to 40) for long entries.

(Default: 10)

Lower values indicate stronger oversold conditions.

RSI Momentum Threshold: Sets the minimum RSI momentum change (1 to 15) to trigger entries.

(Default: 14)

Adjusts the sensitivity to price momentum.

Volume Multiplier: Multiplies the volume moving average to filter high-volume bars (1.0 to 3.0).

(Default: 1)

Higher values require stronger volume confirmation.

Volume MA Length: Sets the lookback period for the volume moving average (5 to 50).

(Default: 13)

Influences the volume trend sensitivity.

Take Profit %: Sets the profit target as a percentage of the entry price (0.1 to 10.0).

(Default: 4.15)

Determines when to close a winning trade.

Stop Loss %: Sets the loss limit as a percentage of the entry price (0.1 to 6.0).

(Default: 1.85)

Protects against significant losses.

Trailing Stop %: Sets the trailing stop distance as a percentage (0.1 to 4.0).

(Default: 2.55)

Locks in profits as the price moves favorably.

Visual Features

Exit Levels: Take profit (green), fixed stop loss (red), and trailing stop (orange) levels are plotted when in a position.

Performance Table: Displays win rate, total trades, and net profit in the top-right corner.

How to Use

Add the strategy to your chart in TradingView.

Adjust the input settings based on the cryptocurrency and timeframe you’re trading.

Monitor the plotted exit levels for trade management.

Use the performance table to assess the strategy’s performance over time.

Notes

Test the strategy on a demo account or with historical data before live trading.

The strategy is optimized for short-term scalping; adjust settings for longer timeframes if needed.

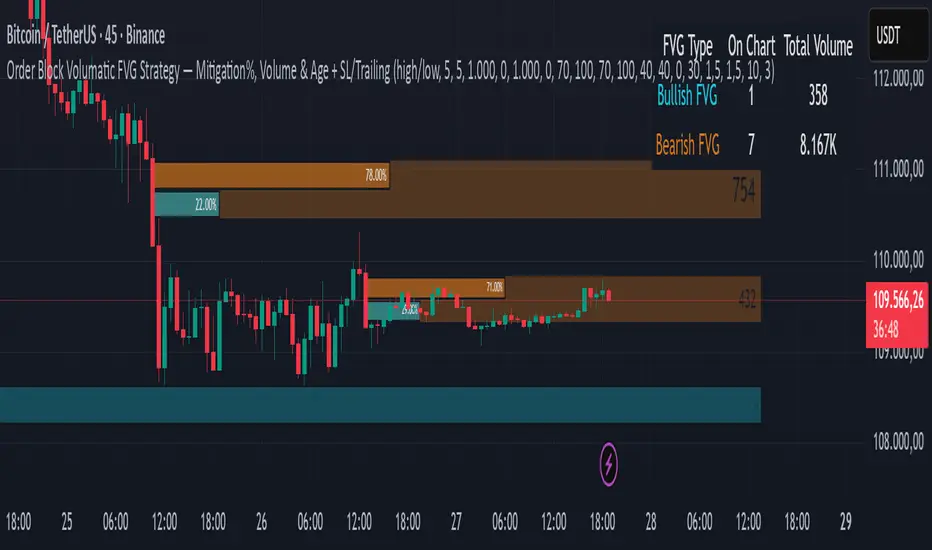

Order Block Volumatic FVG StrategyInspired by: Volumatic Fair Value Gaps —

License: CC BY-NC-SA 4.0 (Creative Commons Attribution–NonCommercial–ShareAlike).

This script is a non-commercial derivative work that credits the original author and keeps the same license.

What this strategy does

This turns BigBeluga’s visual FVG concept into an entry/exit strategy. It scans bullish and bearish FVG boxes, measures how deep price has mitigated into a box (as a percentage), and opens a long/short when your mitigation threshold and filters are satisfied. Risk is managed with a fixed Stop Loss % and a Trailing Stop that activates only after a user-defined profit trigger.

Additions vs. the original indicator

✅ Strategy entries based on % mitigation into FVGs (long/short).

✅ Lower-TF volume split using upticks/downticks; fallback if LTF data is missing (distributes prior bar volume by close’s position in its H–L range) to avoid NaN/0.

✅ Per-FVG total volume filter (min/max) so you can skip weak boxes.

✅ Age filter (min bars since the FVG was created) to avoid fresh/immature boxes.

✅ Bull% / Bear% share filter (the 46%/53% numbers you see inside each FVG).

✅ Optional candle confirmation and cooldown between trades.

✅ Risk management: fixed SL % + Trailing Stop with a profit trigger (doesn’t trail until your trigger is reached).

✅ Pine v6 safety: no unsupported args, no indexof/clamp/when, reverse-index deletes, guards against zero/NaN.

How a trade is decided (logic overview)

Detect FVGs (same rules as the original visual logic).

For each FVG currently intersected by the bar, compute:

Mitigation % (how deep price has entered the box).

Bull%/Bear% split (internal volume share).

Total volume (printed on the box) from LTF aggregation or fallback.

Age (bars) since the box was created.

Apply your filters:

Mitigation ≥ Long/Short threshold.

Volume between your min and max (if enabled).

Age ≥ min bars (if enabled).

Bull% / Bear% within your limits (if enabled).

(Optional) the current candle must be in trade direction (confirm).

If multiple FVGs qualify on the same bar, the strategy uses the most recent one.

Enter long/short (no pyramiding).

Exit with:

Fixed Stop Loss %, and

Trailing Stop that only starts after price reaches your profit trigger %.

Input settings (quick guide)

Mitigation source: close or high/low. Use high/low for intrabar touches; close is stricter.

Mitigation % thresholds: minimal mitigation for Long and Short.

TOTAL Volume filter: skip FVGs with too little/too much total volume (per box).

Bull/Bear share filter: require, e.g., Long only if Bull% ≥ 50; avoid Short when Bull% is high (Short Bull% max).

Age filter (bars): e.g., ≥ 20–30 bars to avoid fresh boxes.

Confirm candle: require candle direction to match the trade.

Cooldown (bars): minimum bars between entries.

Risk:

Stop Loss % (fixed from entry price).

Activate trailing at +% profit (the trigger).

Trailing distance % (the trailing gap once active).

Lower-TF aggregation:

Auto: TF/Divisor → picks 1/3/5m automatically.

Fixed: choose 1/3/5/15m explicitly.

If LTF can’t be fetched, fallback allocates prior bar’s volume by its close position in the bar’s H–L.

Suggested starting presets (you should optimize per market)

Mitigation: 60–80% for both Long/Short.

Bull/Bear share:

Long: Bull% ≥ 50–70, Bear% ≤ 100.

Short: Bull% ≤ 60 (avoid shorting into strong support), Bear% ≥ 0–70 as you prefer.

Age: ≥ 20–30 bars.

Volume: pick a min that filters noise for your symbol/timeframe.

Risk: SL 4–6%, trailing trigger 1–2%, distance 1–2% (crypto example).

Set slippage/fees in Strategy Properties.

Notes, limitations & best practices

Data differences: The LTF split uses request.security_lower_tf. If the exchange/data feed has sparse LTF data, the fallback kicks in (it’s deliberate to avoid NaNs but is a heuristic).

Real-time vs backtest: The current bar can update until close; results on historical bars use closed data. Use “Bar Replay” to understand intrabar effects.

No pyramiding: Only one position at a time. Modify pyramiding in the header if you need scaling.

Assets: For spot/crypto, TradingView “volume” is exchange volume; in some markets it may be tick volume—interpret filters accordingly.

Risk disclosure: Past performance ≠ future results. Use appropriate position sizing and risk controls; this is not financial advice.

Credits

Visual FVG concept and original implementation: BigBeluga.

This derivative strategy adds entry/exit logic, volume/age/share filters, robust LTF handling, and risk management while preserving the original spirit.

License remains CC BY-NC-SA 4.0 (non-commercial, attribution required, share-alike).

StratNinjaTable - VerticalA Pine Script v6 indicator that displays a vertical table with key The Strat data and supporting metrics.

✦ Table Structure:

Overview:

Ticker – the stock symbol.

TF – the chart’s main timeframe.

MFI – Money Flow Index with selectable timeframe.

ATR – Average True Range with color coding:

Green – below 3%.

Yellow – between 3% and 6%.

Red – above 6%.

Timeframes:

Displayed vertically (5m, 15m, 1H, D, W, M, etc.).

Each shows the current bar type according to The Strat (1, 2U, 2D, 3).

Text color reflects candle direction (green = close above open, red = close below open).

Includes a countdown timer to bar close.

Fundamentals:

Market Cap – in billions.

Sector – stock sector.

SMA20 Δ – distance from the 20-period SMA (in %).

Avg Volume (30d) – average 30-day volume (in millions).

✦ Adjustments Made:

Removed the Strat Pattern section completely.

Removed the DIR column – direction is now represented by Strat cell text color.

Reordered Overview section: Ticker → TF → MFI → ATR.

ATR now has three levels of coloring (Green/Yellow/Red) for >3% and >6%

The Maker StrategyDESCRIPTION

The Maker Strategy is a trend-following system built around exponential moving averages (EMAs). By analyzing the alignment of multiple EMAs, the strategy identifies strong bullish or bearish momentum and generates precise entry signals. This method is designed to capture sustained trends while filtering out sideways or noisy market conditions.

USER INPUTS :

• EMA 1 Length (Default: 30)

• EMA 2 Length (Default: 35)

• EMA 3 Length (Default: 40)

• EMA 4 Length (Default: 45)

• EMA 5 Length (Default: 50)

• EMA 6 Length (Default: 60)

LONG CONDITION :

A long signal is triggered when all EMAs are perfectly aligned in ascending order:

EMA1 > EMA2 > EMA3 > EMA4 > EMA5 > EMA6

SHORT CONDITION :

A short signal is triggered when all EMAs are perfectly aligned in descending order:

EMA1 < EMA2 < EMA3 < EMA4 < EMA5 < EMA6

WHY IT IS UNIQUE:

Unlike traditional EMA crossover systems that rely on just 2 or 3 moving averages, The Maker Strategy uses 6 EMAs in sequence. This ensures that trades are only taken when there is clear and strong market momentum. The approach minimizes false signals in ranging markets and focuses on capturing trends with higher probability setups.

HOW USER CAN BENEFIT FROM IT :

• Clear entry alerts for both long and short positions.

• Visual confirmation through candle coloring and EMA band fills.

• Works on multiple timeframes and instruments (stocks, forex, crypto, indices).

• Helps traders stay on the right side of the trend while avoiding whipsaws.

• A simple yet effective tool for those who want a disciplined, rules-based strategy.

RSI Momentum Trend MM with Risk Per Trade [MTF]This is a comprehensive and highly customizable trend-following strategy based on RSI momentum. The core logic identifies strong directional moves when the RSI crosses user-defined thresholds, combined with an EMA trend confirmation. It is designed for traders who want granular control over their strategy's parameters, from signal generation to risk management and exit logic.

This script evolves a simple concept into a powerful backtesting tool, allowing you to test various money management and trade management theories across different timeframes.

Key Features

- RSI Momentum Signals: Uses RSI crosses above a "Positive" level or below a "Negative" level to generate trend signals. An EMA filter ensures entries align with the immediate trend.

- Multi-Timeframe (MTF) Analysis: The core RSI and EMA signals can be calculated on a higher timeframe (e.g., using 4H signals to trade on a 1H chart) to align trades with the larger trend. This feature helps to reduce noise and improve signal quality.

Advanced Money Management

- Risk per Trade %: Calculate position size based on a fixed percentage of equity you want to risk per trade.

- Full Equity: A more aggressive option to open each position with 100% of the available strategy equity.

Flexible Exit Logic: Choose from three distinct exit strategies to match your trading style

- Percentage (%) Based: Set a fixed Stop Loss and Take Profit as a percentage of the entry price.

- ATR Multiplier: Base your Stop Loss and Take Profit on the Average True Range (ATR), making your exits adaptive to market volatility.

- Trend Reversal: A true trend-following mode. A long position is held until an opposite "Negative" signal appears, and a short position is held until a "Positive" signal appears. This allows you to "let your winners run."

Backtest Date Range Filter: Easily configure a start and end date to backtest the strategy's performance during specific market periods (e.g., bull markets, bear markets, or high-volatility periods).

How to Use

RSI Settings

- Higher Timeframe: Set the timeframe for signal calculation. This must be higher than your chart's timeframe.

- RSI Length, Positive above, Negative below: Configure the core parameters for the RSI signals.

Money Management

Position Sizing Mode

- Choose "Risk per Trade" to use the Risk per Trade (%) input for precise risk control.

- Choose "Full Equity" to use 100% of your capital for each trade.

- Risk per Trade (%): Define the percentage of your equity to risk on a single trade (only works with the corresponding sizing mode).

SL/TP Calculation Mode

Select your preferred exit method from the dropdown. The strategy will automatically use the relevant inputs (e.g., % values, ATR Multiplier values, or the trend reversal logic).

Backtest Period Settings

Use the Start Date and End Date inputs to isolate a specific period for your backtest analysis.

License & Disclaimer

© waranyu.trkm — MIT License.

This script is for educational purposes only and should not be considered financial advice. Trading involves significant risk, and past performance is not indicative of future results. Always conduct your own research and risk assessment before making any trading decisions.

BE-Fib Channel 2 Sided Trading█ Overview:

"BE-Fib Channel 2 Sided Trading" indicator is built with the thought of 2 profound setups named "Cup & Handle (C&H)" and "Fibonacci Channel Trading (FCT)" with the context of "day trading" or with a minimum holding period.

█ Similarities, Day Trading Context & Error Patterns:

While the known fact is that both C&H and FCT provide setups with lesser risk with bigger returns, they both share the similar "Base Pattern".

Note: Inverse of the above Image shall switch the setups between long vs short.